Sparking Conversation & Discovery

-

4 Bulletproof Business Failsafe Ventures

In the ever-evolving world of entrepreneurship, the mantra “nine out of ten businesses fail” has become a daunting reality for many aspiring entrepreneurs. However, the landscape is shifting, and not all businesses are created equal when it comes to their chances of survival. In this comprehensive guide, we will uncover the four business models that…

-

Embrace the Journey: 40 Life Lessons from a Seasoned Blogger

As we navigate the ever-changing landscape of life, it’s important to reflect on the wisdom we’ve accumulated along the way. In this comprehensive article, a seasoned blogger shares 40 powerful life lessons that he’s learned by the age of 40. From the insights on relationships and personal development to the practical tips on productivity and…

-

How to Start a Profitable Blue Collar Business With Low Startup Costs

For many people, the appeal of starting their own business comes from the prospect of high earnings and independence. However, concerns about substantial startup costs often deter would-be entrepreneurs from taking the leap. Fortunately, there are plenty of blue collar business ideas that can generate impressive profits without requiring a huge initial investment. This comprehensive…

-

The Hidden Technology Inside Nespresso Coffee Pods

Nespresso completely changed the way people drink and think about espresso when it launched its innovative coffee pod system in the late 1980s. The convenience and speed of being able to make high-quality espresso drinks at home captivated consumers and transformed Nestle into a coffee powerhouse. By 2022, Nespresso was generating over 6 billion CHF…

-

How Hotel Rooms Are Assigned: An Inside Look Into the Complex World of Hotel Room Allocations

Have you ever arrived at a hotel, settled into your room, then decided you wanted to extend your stay only to be told you needed to switch rooms? It’s a frustrating experience, but there’s actually a fascinating science behind how hotels assign their limited rooms. As someone who has worked at hotels of all sizes,…

-

Proactive Steps to Take for an Upcoming Recession

A recession can happen at any time and catch many people off guard. Being proactive and prepared is key to navigating an economic downturn. In this article, we will explore six practical steps you can take now to recession-proof your finances. What Defines a Recession A recession is typically defined as two or more consecutive…

-

How Understanding the Psychology of Money Can Help You Become Financially Free

Money. It’s something we all need and want, yet it’s often a source of stress and discomfort. Beyond just dollars and cents, our relationship with money has deep psychological roots. In this article, we’ll explore some fascinating insights from psychology that can transform the way you manage your finances. You’ll learn about emotional spending, the…

-

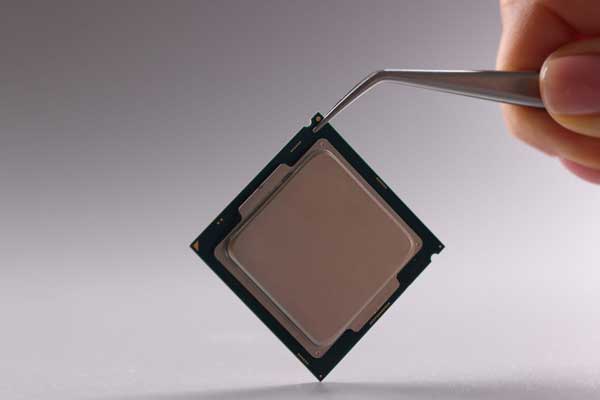

Arm: The Essential Player Powering Your Smartphone, Laptop and More

The company behind the chip technology in billions of devices takes center stage. There’s a company nearly every chipmaker relies on that doesn’t actually make anything tangible. Yet its blockbuster IPO in September valued it above $54 billion. Arm is the most pervasive CPU or brain in the history of modern electronics. Understanding what Arm…

-

Escape the 9-to-5: How to Achieve Financial Independence According to Robert Kiyosaki

Have you ever dreamed of not being tied to a traditional job and having the freedom to live life on your own terms? Many assume it’s an unrealistic fantasy, but financial guru Robert Kiyosaki argues it’s very attainable for those willing to take control of their financial life. In his teachings, Kiyosaki provides a roadmap…

-

The Fascinating History Behind Why Cash is King

Money makes the world go ’round. Almost everything we do each day revolves around using money in some way. We work to earn it, we spend it when we shop, and we save and safeguard our stash of money. But why do we dedicate so much of our lives to money? What is it that…

-

China’s Xiaomi Unveils Groundbreaking Surge OS Operating System – A Major Blow to US Tech Sanctions

China has made major strides in developing its domestic tech industry and reducing reliance on American firms. Xiaomi’s introduction of its own operating system Surge OS deals a serious blow to US efforts to curb Chinese tech giants through sanctions. This launch signifies monumental progress for China’s digital sector. Xiaomi Surge OS Supplants Google’s Android…

-

The Fascinating History Behind Why Half the World Uses 110 Volts and the Other Half Uses 220 Volts

Have you ever wondered why some countries use 110 volts electricity while others use 220 volts? This difference actually stems from the early days of electrical systems pioneered by Thomas Edison in the late 1800s. Edison’s Quest to Light Up New York City It all started in 1878 when Thomas Edison, then just 31 years…